Making Sense of January’s Market Volatility

Monthly Market Summary

The S&P 500 Index produced a -5.3% total return during January, outperforming the Russell 2000 Index’s -9.5% total return.

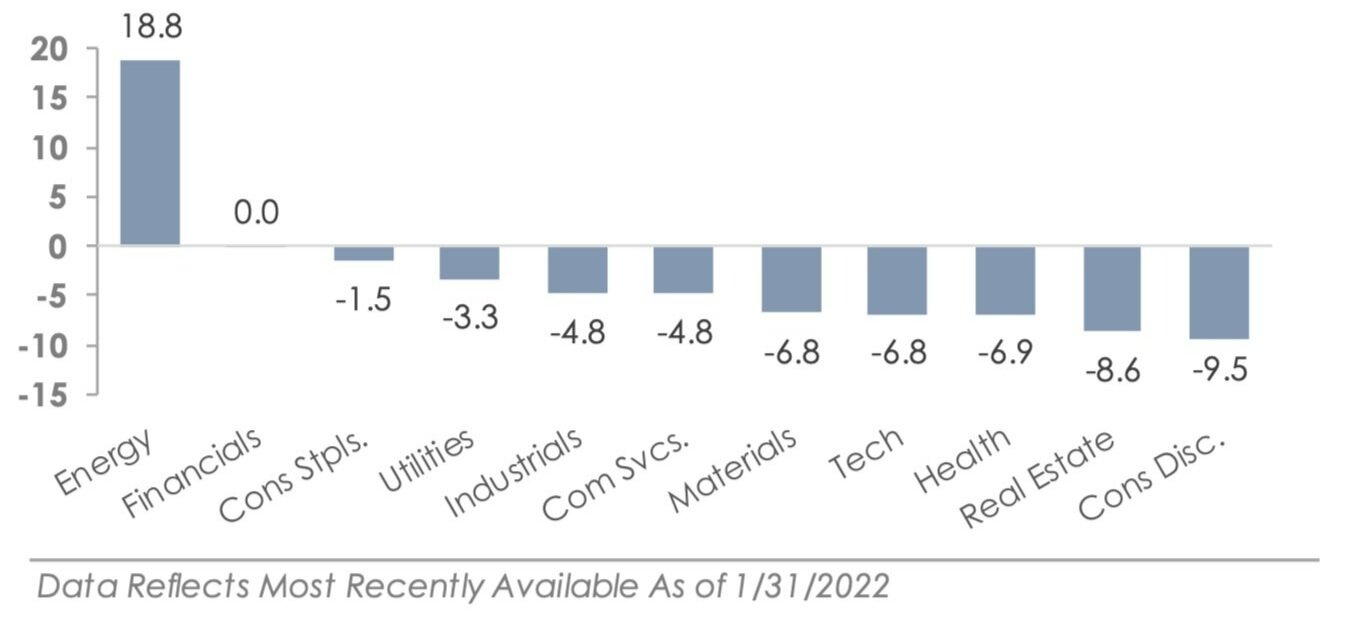

The energy sector was the only sector to trade higher, returning +18.8% as oil prices rose +17.4%. Financials were the second-best sector, returning +0.0% as interest rates rose. Consumer Discretionary was the worst-performing sector with a -9.5% return, followed by Real Estate’s -8.6% return and Health Care’s -6.9% return.

Corporate investment grade bonds generated a -3.6% total return and underperformed corporate high yield bonds’ -2.7% total return.

The MSCI EAFE Index of global developed market stocks returned -3.6% during January, underperforming the MSCI Emerging Market Index’s +0.0% return.

US Sector Returns for January 2022 (%)

Market Volatility Increases as Federal Reserve Responds to Surging Inflation

The Federal Reserve is moving closer to addressing high inflation. The U.S. central bank is preparing to tighten monetary policy by ending its monthly bond purchases and raising interest rates. Monthly asset purchases were initiated during the pandemic as a way to inject money into the economy by buying bonds, allowing lenders to go back out and lend again. In addition, interest rates were lowered to decrease financing and debt servicing costs. Together, bond purchases and low-interest rates stimulated demand during the depths of the pandemic. However, the two monetary policies appear to have done too good job stimulating demand. Inflation rose +7% year-over-year during 2021, the fastest pace since 1982. Now, the Federal Reserve is preparing to reverse the two policies and tighten financial conditions to dampen strong demand.

Interest rates rose during January in anticipation of the Federal Reserve’s actions. The 10-year Treasury yield rose +0.27% to end the month at 1.78%, back near January 2020 levels. Rising interest rates led to higher real yields, which is the yield an investor earns after accounting for inflation. Figure 1 on page 2 shows real yields rose during January 2022 after touching a record low in 2021 due to a combination of high inflation and near-zero interest rates. 2021’s deeply negative real yields caused investors to turn to riskier investments to generate positive after-inflation returns.

Investors Prepare for Tighter Financial Conditions

There was a broad rotation in the equity and credit markets during January. De-risking was a prominent theme as real yields rose and investors adjusted portfolios. The S&P 500 and Russell 2000 indices traded lower, and all but one of the eleven S&P 500 sectors traded lower. Trading action was volatile at times, with large intra-day reversals. The S&P 500 swung more than 2% between the intra-day high and intra-day low each day from January 20th-28th, with a 4.6% intra-day swing on January 24th. The increased volatility is being attributed to changing Federal Reserve policy.

There were multiple performance trends worth mentioning. January was S&P Growth’s fourth biggest month of underperformance since January 1994. Growth stocks are valued based on their future earnings, and rising interest rates tend to decrease the price-to-earnings multiple markets place on those earnings. In the credit markets, bonds generated negative returns and did not offer protection from the equity market selloff. Finally, cryptocurrencies plunged during January, with bitcoin falling -by 19.4% as speculative assets saw aggressive selling.

2022 is off to a difficult start, but it is important to keep the big picture in mind. The S&P 500 experienced an average maximum pullback of -14.2% since 1986. For comparison, 2021’s maximum pullback was -5.2% or almost 10% below the average. The data indicates that 2021 was the exception, not the rule. Volatility is the price of admission to investing and will continue to impact portfolios. Experiencing market selloffs is unpleasant, but annual returns historically finish the year well above the maximum drawdown level.

Our Insights