Solid Economic Data Lifts Interest Rates

Photo Credit: Arvind Vallabh, Unsplash

Weekly Market Recap for October 20, 2023

Equities traded lower this week, with Large and Small caps producing similar returns while the Nasdaq underperformed. Factors exhibited mixed performance, with Low Volatility and Value outperforming while Growth and High Beta lagged. Energy was the top-performing sector as oil prices traded higher, and defensive sectors outperformed cyclical sectors. Bonds traded lower as interest rates reversed higher, with longer duration bonds underperforming.

S&P 500 Index (Last 12 Months)

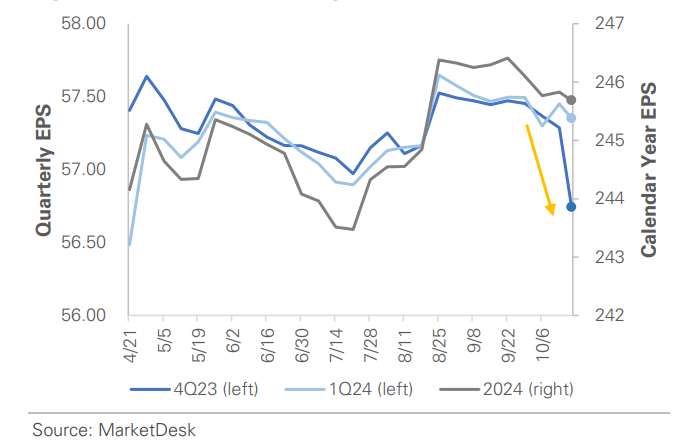

S&P 500 Quarterly Earnings Per Share (EPS) Estimates

Analysts Are Revising 4Q23 EPS Estimates Lower

Solid Economic Data Lifts Interest Rates

Last week, multiple Fed speakers suggested that rising long-term yields might reduce the need for additional rate hikes, which caused yields to decline. However, interest rates reversed higher this week after strong retail sales and industrial production data highlighted the U.S. economy's continued resilience. U.S. retail sales rose 0.7% m/m in September, with upward revisions for July and August. The index for industrial production rose 0.3% m/m to 103.6 in September, its highest level since December 2018. The data points to robust 3Q23 GDP growth, with the Atlanta Fed's 3Q23 GDPNow Forecast rising to 5.4%, marking the most robust growth since 4Q21.

US Retail Sales

Retail sales data highlights consumer resistance

Market Sticks with No Rate Hike Forecast

The solid economic data, while making the case for more rate hikes, did not sway the market's expectations for further rate hikes. The CME's FedWatch Tool shows that the rate hike probability at the November 1 meeting is 6.5%. The question around interest rates is shifting from 'how high' to 'how long'.

Rate Hikes Only Impact Rate Sensitive Industries

This is an obvious statement, but it underscores the limited impact of the Fed's actions thus far. Consider the following housing data from this week: (1) homebuilder sentiment weakened for a third consecutive month; (2) building permits and housing starts are significantly below their pandemic peaks; and (3) existing home sales are below the pandemic trough, nearing levels from late 2010. The housing weakness is occurring as mortgage rates top 8%, indicating that higher rates are slowing activity. However, robust retail sales and industrial production data suggest the broader economy remains resilient. The Fed's primary challenge is that borrowers locked in low-interest rates during the pandemic. Higher interest rates simply aren't impacting non-borrowers.

Quantitative Tightening Unlikely to End Near-Term

In a speech this week, Fed President Waller reaffirmed his view on QT. He maintained that the banking system's optimal reserves would amount to ~$2.5 trillion, which he defines as both commercial bank reserves and the Fed's reverse repurchase program (RRP). Reserves totaled $3.25 trillion at the end of August, and RRP sits at $1.15 trillion as of this week. Based on Waller's definition, there are currently $4.4 trillion in "reserves". QT's current $95 billion monthly pace could run for another 20 months until it reaches Waller's target.

Citi's CEO Provides Succinct Macro Snapshot

We want to end this market update with a quick around-the-world summary of the macroenvironment through the eyes of Citi Bank's CEO Jane Fraser.

"The global macro backdrop remains a story of desynchronization. In the US, recent data implies a soft landing, but history would suggest otherwise and we are seeing some cracks in the lower-FICO consumers. In the euro area and the UK, the picture has turned distinctly more negative. The summer weakness in industrial economies is spreading south, and the weight of structurally higher labor and energy costs suggests a more enduring competitiveness challenge for that region. China's economy may have reached a cyclical bottom supported by the government's modest stimulus efforts, but it still has to work through weak sentiment, youth unemployment, and the pain in its property market. All of these macro dynamics have clearly impacted client sentiment. September is always a busy month seeing clients, and I'm struck how consistently CEOs are less optimistic about 2024 than a few months ago. The shift in the rates question from how high to how long has catalyzed more client activity, however. Corporates have stopped waiting for rates to come down and are beginning to access the debt capital markets around the globe."

Important Disclosures

This material is provided for general and educational purposes only and is not investment advice. Your investments should correspond to your financial needs, goals, and risk tolerance. Please consult an investment professional before making any investment or financial decisions or purchasing any financial, securities, or investment-related service or product, including any investment product or service described in these materials.

Our Insights