4th Quarter Recap and 2025 Outlook

Photo Credit: Getty, Unsplash

Key Updates on the Economy & Markets

There was no shortage of market-moving events in Q4. The stock market opened the quarter with a slow start in October, but the presidential election’s outcome triggered a broad rally in November. The rally faded as the year ended, although the S&P 500 traded only a few percentage points below its all-time high. The credit market was equally active in Q4, with the Federal Reserve cutting rates by another -0.50%. However, the significant development was the changing 2025 outlook. Both the Fed and the market expect fewer rate cuts in 2025 compared to the end of Q3, which resulted in a sharp rise in Treasury yields in Q4. This post recaps the fourth quarter, looks back on the 2024 stock market rally, provides an update on the economy and the Fed’s rate-cutting cycle, and looks ahead to 2025.

Looking Back on the 2024 Stock Market Rally

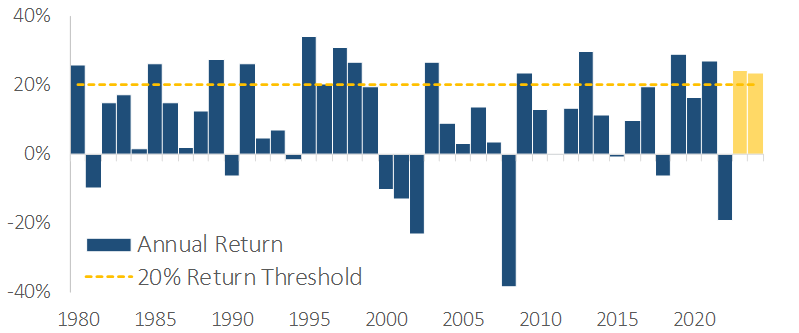

The past two years have been remarkable for investors, with the S&P 500 delivering strong returns in back-to-back years. The three charts below take a closer look at the stock market’s rally in 2024, a year in which the S&P 500 set more than 55 new all-time highs. The top chart, which graphs the S&P 500’s return for each calendar year since 1980, shows the index posted gains of over +20% in 2023 and 2024. It marked the first time in the 4 years from 1995 to 1998, and like the late 1990s, large-cap technology stocks played a significant role in the S&P 500’s gains.

The second chart shows the 2024 price returns of seven ETFs, each reflecting exposure to companies of different market cap sizes. The chart reveals a significant gap between the returns of large-cap and small-cap stocks in 2024. The top bar tracks the Magnificent 7, which includes Microsoft, Apple, Alphabet, Meta, Amazon, Nvidia, and Tesla. These seven companies, which now account for over 33% of the S&P 500, returned over +60%. When the group expands from the Magnificent 7 to the 50 largest S&P 500 stocks, the return falls to +32%, still impressive but around half of the Magnificent 7’s return. Broadening the group further to include all S&P 500 companies reduces the index return to approximately +23%, and weighting companies equally rather than by market capitalization lowers the return to +11%.

The key takeaway is that the largest companies contributed significantly to the S&P 500’s return in 2024. Smaller companies delivered solid returns around +10%, but they underperformed relative to the larger companies. An index of mid-cap stocks returned +12%, while small-cap and micro-cap stocks returned +10% and +12%, respectively.

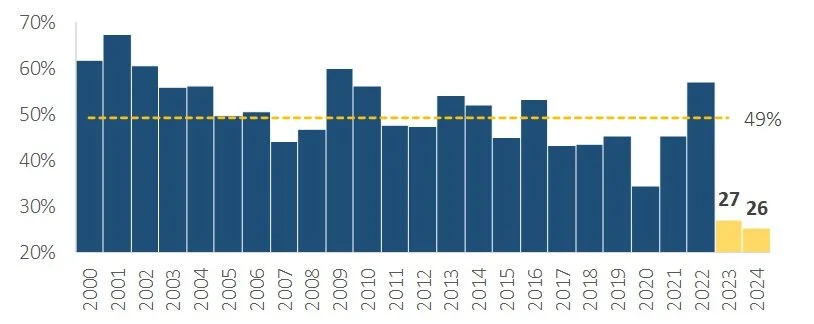

The concentrated stock market rally, driven by the outperformance of the largest companies, led to an unusual outcome. The bottom chart tracks the percentage of S&P 500 companies outperforming the index each calendar year. For the second consecutive year, fewer than 30% of S&P 500 companies beat the index in 2024. This is significantly below the average of 49% since 2000 and highlights the dominance of the largest companies in 2024.

S&P 500 Calendar Year Returns Since 1980

Source: Standard & Poors

2024 Returns by Market Cap Size

Source: Standard & Poors

Percentage of Stocks Outperforming the S&P 500

Source: Standard & Poors

Data Highlights the US Economy’s Resilience

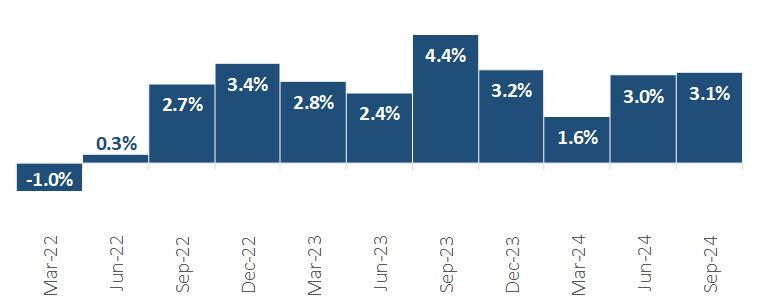

The US economy has consistently defied expectations of a slowdown since the Fed started raising interest rates in March 2022. Economists and market participants initially expected growth to slow as the Fed raised interest rates. However, it has been nearly three years since the Fed’s first rate hike, and the economy continues to grow at an above-trend rate. While higher rates have slowed housing demand and weighed on business investment, the US economy has defied expectations with solid GDP growth. The chart below shows the US economy grew at a +3.1% annualized pace in 3Q24, marking the third quarter in the past four with growth above +3%.

Real GDP Growth (% q/q)

Source: Federal Reserve, US Bureau of Economic Analysis, US Census Bureau

The following two charts show key drivers of economic growth since early 2022. The middle chart tracks the contribution of personal consumption expenditures (i.e., consumer spending) to US GDP growth. Despite high interest rates, consumer spending has remained a steady growth driver in recent quarters. Multiple factors have increased household net worth and bolstered consumers’ financial strength, including record-high stock prices, rising home values, and solid wage growth. Additionally, many borrowers locked in low interest rates during the pandemic, which has made the US economy less sensitive to rising interest rates this cycle.

US Personal Consumption Expenditures, Contribution to GDP (% q/q)

Source: Federal Reserve, US Bureau of Economic Analysis, US Census Bureau

The bottom chart shows the surge in manufacturing-related construction in recent years. Manufacturing construction was relatively modest for a long time, as most activity was outsourced to China, Mexico, and elsewhere. However, that changed in late 2021, when Congress passed trillions in new spending on infrastructure, green energy, and subsidies to incentivize US manufacturing. These spending bills have supported the US economy and created a boom in manufacturing semiconductors, electric vehicles, batteries, and solar panels. The result is a surge in manufacturing-related construction, the largest on record, as companies build new warehouses, industrial facilities, and semiconductor plants. The artificial intelligence industry’s emergence has provided another catalyst, as companies like Microsoft, Amazon, and Meta spend billions on data centers, information processing equipment like semiconductors, and energy production to meet growing power demand.

US Spending on Manufacturing-Related Construction

Source: Federal Reserve, US Bureau of Economic Analysis, US Census Bureau

Economic growth is forecast to slow but remain solid next year, driven by the Trump administration’s pro-growth policies. The new administration’s policy agenda focuses on extending the 2017 tax cuts, reducing industry regulations, and boosting domestic manufacturing through targeted incentives. These measures can stimulate capital expenditures, expand manufacturing capacity, and attract foreign investment to the US.

An Update on the Fed’s Interest Rate-Cutting Cycle

The Fed continued its rate-cutting cycle in Q4, lowering interest rates by -0.25% at the November and December meetings for a total of -0.50%. The two -0.25% rate cuts were well-telegraphed by the Fed and widely expected, but the big development in Q4 was the changing outlook for 2025. Despite the two rate cuts, Fed Chair Jerome Powell and other Fed presidents indicated they are not hurrying to cut rates further. The change in tone follows the US economy’s recent strength, which has caused the Fed to re-examine the need for additional rate cuts.

Recent economic strength has also led the market to re-evaluate its rate-cut forecast. This dynamic can be seen in the bond market, where longer-maturity Treasury yields have risen sharply since the first rate cut in September. The chart below shows the 10-year Treasury yield against the federal funds rate, which is the interest rate the Fed adjusts to set monetary policy. Since the first rate cut in September, the federal funds rate has decreased by -1.00%. While the Fed controls shorter-maturity interest rates, the market has more control over longer-maturity interest rates. Over the same period, the 10-year Treasury yield has had the opposite reaction: rising by nearly +1.00%.

US 10-Year Treasury Yield vs Federal Funds Rate

Source: US Treasury, Federal Reserve

What caused Treasury yields to rise as the Fed cut interest rates?

Two key data points contributed to the Fed’s decision to start cutting rates in September: falling inflation and rising unemployment. Inflation declined from 3.3% in July 2023 to 2.6% in August 2024, while unemployment rose from 3.5% to 4.3%. The two trends caused the Fed to shift its focus from lowering inflation to supporting the labor market. However, since the Fed started cutting, the trends have reversed. Inflation progress has stalled since September, and unemployment has declined to 4.2%. Heading into 2025, the Fed and the market have similar rate cut expectations: approximately -0.50% in cuts for the entire year. The question is whether they are placing too much emphasis on recent trends and underestimating the need for rate cuts. As the Fed and the market saw in 2024, forecasting Fed policy is difficult, especially in this cycle.

Equity Market Recap – Stocks End the Year Higher

The stock market ended Q4 higher, but the path included periods of volatility. In October, the S&P 500 ended its five-month winning streak, with most of the equity market finishing slightly lower. The sluggishness occurred as Treasury yields rose after the Fed’s first rate cut in September, suggesting the sharp rise in yields may have played a role in October’s market action. However, stocks rebounded in subsequent months.

The quick and decisive election outcome in November became a tailwind for stocks. Investor enthusiasm fueled the post-election rally, with stocks trading higher in anticipation of tax cuts, deregulation, and US-focused trade policies aimed at benefiting US companies. Small caps led the way during the broad market rally, with the Russell 2000 rising +11% in November to set a record high. Bank stocks were another popular post-election trade as investors priced in expectations for financial deregulation and strong economic growth. Industrial stocks saw broad-based strength in anticipation of the Trump administration’s pro-growth policies and protectionist policies, which could spark an industrial renaissance in the US By the end of November, the S&P 500’s year-to-date return surpassed +26%, putting the index on track for consecutive gains of more than +20%.

The market’s excitement cooled in December, with the S&P 500 trading sideways and ending the month lower. Under the surface, a familiar trend from earlier in the year impacted returns, with smaller companies underperforming larger ones by a wide margin. The Russell 2000 Index was hit hardest, falling -8.4% and giving back most of its post-election gains. Value stocks also traded lower in December, with the Russell 1000 Value Index declining by -6.8%. In contrast, the Magnificent 7 stocks discussed earlier gained more than +5%.

Shifting the focus to global markets, international stocks underperformed US stocks in Q4. The MSCI Emerging Market Index returned -7.2%, while the MSCI EAFE Index of developed market stocks returned -8.3%. Both major international equity indices underperformed the S&P 500 by nearly -10% due to currency headwinds (i.e., a stronger US dollar) and the outperformance of US mega-caps. Looking ahead to 2025 for international markets, the potential for tariffs under the Trump administration is creating significant uncertainty across several global regions.

Credit Market Recap – Bonds Trade Lower as Interest Rates Rise Throughout the Quarter

The sharp rise in Treasury yields weighed on bond returns in Q4. The biggest differentiator within the bond market was duration, or the sensitivity of a bond’s price to interest rate movements. High-yield corporate bonds produced a total return of -0.1% due to their lower sensitivity to rising interest rates and higher absolute yields. In contrast, investment-grade bonds returned -4% as increasing yields had a bigger impact on their longer maturities. Excluding interest received and only looking at price returns, an index of investment-grade corporate bonds posted its most significant quarterly loss since Q3 2022.

Full-year credit returns highlight the key themes that shaped the bond market throughout 2024. Higher-quality bonds like US Treasuries, corporate investment-grade, and mortgage-backed securities underperformed as the market debated and ultimately lowered its rate-cut expectations. In contrast, lower-quality bonds outperformed as economic growth and corporate fundamentals remained solid. Corporate credit spreads, which measure the difference in yield between two bonds with a similar maturity but different credit quality, steadily tightened throughout the year. This boosted lower-quality bonds in 2024 but has left credit spreads near their lowest levels in decades. For context, the US high-yield corporate credit spread is near its lowest level since 2007, meaning investors receive less yield in return for taking credit risk.

2025 Outlook – Key Themes to Watch

The S&P 500’s steady climb in 2024 reflects the market’s growing confidence. Investors are optimistic about the artificial intelligence industry’s growth potential. Despite high interest rates, the US economy outperformed expectations, growing at an above-trend rate in three of the past four quarters. The stock market rally intensified after the election in November as investors focused on the incoming administration’s policy agenda. Expectations for tax cuts, deregulation, and energy production fuel hopes for more substantial economic growth. The bond market echoes the equity market’s confidence, and corporate high-yield credit spreads are near their lowest levels in over 15 years.

However, the equity market rally has made broad market indices like the S&P 500 more concentrated and expensive. The question on many minds is whether the momentum can continue in 2025. The S&P 500 currently trades at nearly 22x times its next 12-month earnings estimate, a level not seen outside periods like the late-1990s tech boom and the recent post-COVID recovery, when interest rates were near zero. Investors have shown a willingness to pay higher multiples, but with valuations now at extremes, earnings growth will likely play an essential role in determining the stock market’s path in 2025.

S&P 500 Returns During Bull Markets

The chart above tracks the current bull market, which started in October 2022 and is now in its third year. The current bull market has performed in line with historical norms, but the chart shows that returns often moderate as bull markets mature. This suggests that the market’s focus could shift to fundamentals and earnings as the next catalyst to push markets higher. 2025 is shaping up to be a year where companies will need to deliver on investors’ expectations to justify their high valuations.

Important Disclosures

This material is provided for general and educational purposes only and is not investment advice. Your investments should correspond to your financial needs, goals, and risk tolerance. Please consult an investment professional before making any investment or financial decisions or purchasing any financial, securities, or investment-related service or product, including any investment product or service described in these materials.

Our Insights