Economic Data Highlights Inflation's Stickiness

Photo Credit: Franki Chamaki, Unsplash

Weekly Market Recap for February 23, 2024

This week saw the release of the minutes from the latest Federal Open Market Committee (FOMC) meeting that was held on January 30–31, 2024. The report was full of concerns among Federal Reserve officials about upside risks to inflation, driven by still strong demand. It is also worth noting that the FOMC meeting came before data showed an uptick in January price growth. The report also revealed that only a couple of voting members believed there were risks to keeping rates high for longer. The FOMC minutes were more hawkish than dovish concerning potential near-term monetary policy decisions. On a positive note, Federal Reserve officials noted that banking risks have “receded notably.”

S&P 500 Index

S&P 500 Technical Composite (Last 24 Months)

Producer Prices Rise More Than Forecast

The Producer Price Index rose by +0.3% month over month in January vs the +0.1% consensus estimate. The advance can be traced to a +0.6% rise in Service prices, the most significant increase since +0.8% in July 2023. Hospital outpatient care (+2.2% month over month) was a substantial factor in the increase, with additional increases in portfolio management, legal services, and wholesaling indexes. In contrast, the Goods index declined by -0.2% month over month, its fourth consecutive monthly decline. Most of the Goods decrease was attributable to a -1.7% month over month decline in energy prices. The report continued the prevailing trend, with Services creating inflation and Goods experiencing deflation. The PPI report followed the January CPI report from an earlier week, highlighting inflation's persistence.

Producer Prices Rise More Than Forecast

Import Prices Rise in January

Prices of goods imported into the US rose by +0.8% month over month as the cost of both fuel and nonfuel imports increased. It was the first monthly increase since September 2023 and the most significant increase since +2.9% in March 2022. However, despite the January increase, US import prices fell by -1.3% year over year, the 12th consecutive year-over-year decline. Excluding energy, nonfuel import prices rose by +0.6% month over month, the most significant monthly increase since March 2022. Prices increased across various categories, including consumer goods, capital goods, automotive vehicles, foods, feeds, and beverages. While the price index for nonfuel imports fell by -0.3% year over year, it was the smallest decline since February 2023. The question is whether this trend of falling import prices is reversing. The chart below shows the steady decline in import prices since May 2022, allowing the US to import deflation. This trend of falling import prices likely contributed to the recent decline in inflation, but the January report shows the US cannot necessarily rely on the trend to continue. One interesting data point was import prices by locality: January's rise was tied to Japan, Mexico, and the EU, while import prices from China declined.

Import Prices Post Biggest Increase Since December 2022

Inflation Base Effects?

The market entered 2024, convinced that inflation would return to 2% and the Fed would cut rates by -1.50% to target a lower real interest rate. Both forecasts were optimistic. Last week's inflation reports showed that getting back to 2% will be bumpy with a risk of persistent inflation, and the Fed has already pushed back against the market's rate cut forecast. Previous reports have discussed how rising fiscal deficits, labor strikes, and structural pandemic changes like domestic migration create lingering inflation risk. We believe the Fed would take a more measured approach to cutting rates in the range of -0.75%. The latest inflation data points demonstrate the case for "higher for longer." This, plus the increasing size of Treasury auctions, are two reasons we are not rushing to lock in yields for a Long Duration.

Fed Meeting Minutes

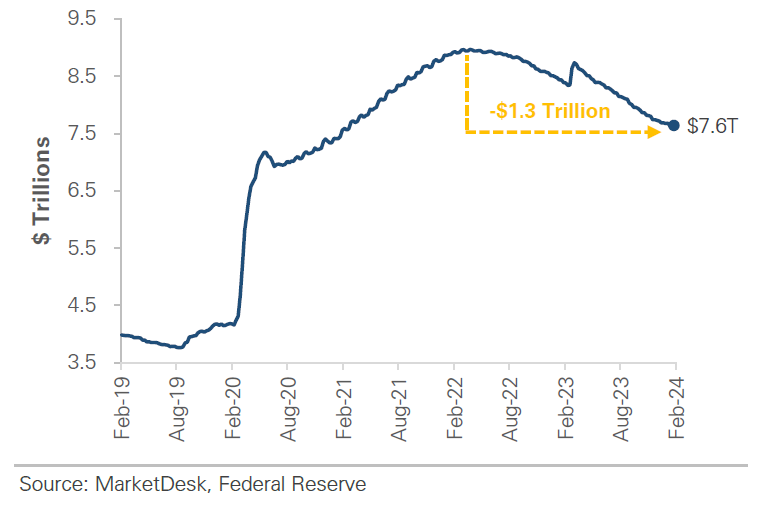

The Fed’s January meeting minutes were released this week, and the takeaways were mostly in line with recent Fedspeak. Officials are debating when to start cutting interest rates, but they want more evidence that inflation is firmly on the path to 2%. There was talk about the risk of cutting too soon, and given last week’s hot inflation data and January’s job gains, this concern is likely higher today. The one theme that stuck out related to the Fed’s balance sheet and discussions around when to slow quantitative tightening. Quantitative Tighting (QT) has been in place for over 1.5 years and shrunk the balance sheet by ~$1.3 trillion, but Fed officials stated that liquidity remains “more than ample.” Our US Net Liquidity Indicator is consistent with the past 3-, 6-, and 12-month changes, ranking in the 72% percentile compared to the last 3 years. The Fed wants to start the discussion, but there’s plenty of liquidity and runway for QT to continue.

QT Shrinks Fed Balance Sheet By $1.3 Trillion

Leading Economic Index Declines for 23rd Consecutive Month

After previously signaling a recession, leading economic data are now turning less negative. From this month's LEI release: "While the declining LEI continues to signal headwinds to economic activity, for the first time in the past two years, six out of its ten components were positive contributors over the past six-month period (ending in January 2024). As a result, the leading index currently does not signal recession ahead. While no longer forecasting a recession in 2024, we do expect real GDP growth to slow to near zero percent over Q2 and Q3." Soft data and traditional leading indicators have struggled to measure the current cycle accurately, but it is starting to suggest the elusive soft landing is now in play. While the outlook for 2024 is improving, there continues to be potential for a slowdown in 2025 and beyond.

Leading Economic Index Declines for 23rd Straight Month

Important Disclosures

This material is provided for general and educational purposes only and is not investment advice. Your investments should correspond to your financial needs, goals, and risk tolerance. Please consult an investment professional before making any investment or financial decisions or purchasing any financial, securities, or investment-related service or product, including any investment product or service described in these materials.

Our Insights