Implications of the US Treasury’s Financing Announcement

US Treasury original seal, dating from before 1968. Photo Credit: Tommano Wang, Unsplash

Weekly Market Recap for November 10, 2023

Federal Reserve officials this week provided additional insight into the central bank's approach to combating inflation and the current state of the US economy. Their remarks closely aligned with Chairman Powell's announcement, which was presented at the recent Fed meeting at the beginning of this month. During both that meeting and the preceding September gathering, the Federal Open Market Committee opted to maintain the stability of short-term interest rates within the range of 5.25% to 5.50%, marking a cumulative increase of five points since March 2022.

S&P 500 Technical Composite (Last 24 Months)

S&P 500 Earnings for Q3

Earnings season is almost over, with almost 90% of S&P 500 companies having reported earnings at this point. 80% have beaten their projected earnings better than the 10-year average of 74%. This season has turned out well because companies expanded their margins and cut costs with the help of falling input costs, slower wage growth, and layoffs of front-line workers in some sectors, such as technology.

S&P 500 Earnings 2023 Q3 Beat Miss Rate

S&P 500 2023 Q3 Year-Over-Year Earnings Growth

With this above-average beat rate, Q3 S&P 500 earnings are now on track to increase 4.1% year over year, which is a five percentage point improvement from expectations.

US Treasury Announcements

Last week, the U.S. Treasury announced its updated borrowing estimates and projected issuance for the next two quarters.

Quarterly Financing Estimate

During the October–December 2023 quarter, Treasury expects to borrow $776 billion, which is $76 billion below its July estimate due to higher projected tax receipts. During the January–March 2024 quarter, Treasury expects to borrow $816 billion. For context, Treasury borrowed $1.01 trillion in the July–September 2023 quarter.

Quarterly Refunding Statement

As expected, the refunding statement reaffirmed that the Treasury intends to increase auction sizes during the next two quarters due to increased fiscal spending. However, the underlying issuance details, or what mixture of bond maturities Treasury plans to sell, grabbed the market's attention. While Treasury plans to increase auction size across all maturities, it will rely more on Treasury bill sales than Treasury bond sales.

The market reacted positively to both the financing and refunding announcements. Investors have been concerned that increased Treasury bond issuance would outpace demand and cause yields to rise on the long end of the curve. The reduced financing estimate and preference to issue Treasury bills over bonds alleviated some of the market's concern about oversupply.

Risk Assets

Risk assets received an immediate boost following the Treasury's refunding statement, which favored bills over bonds. Why? Treasury bills primarily compete with cash and other short-duration bonds. In contrast, Treasury bonds, particularly longer-maturity bonds, compete directly with risk assets such as stocks. Fewer long-duration bonds mean less supply for the market to absorb, which in turn means less selling pressure on risk assets.

Furthermore, decreased Treasury bond issuance neutralizes a portion of quantitative tightening (QT). Usually, the effects of the Fed's reduced bond purchases would impact credit markets, but with the Treasury issuing fewer bonds, the Fed's absence will be less impactful. This only neutralizes QT while the Treasury issues fewer bonds. As the Treasury increases the auction sizes of Treasury bonds in the coming quarters, the Fed's absence will be more impactful.

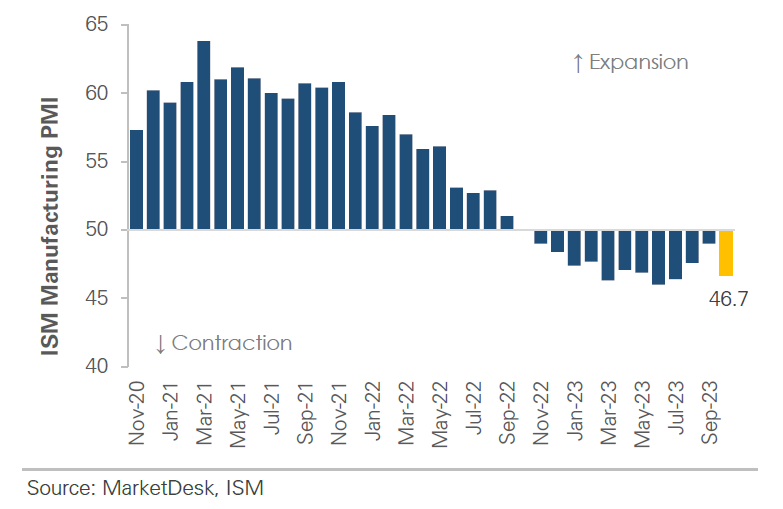

Manufacturing Activity Continues to Contract

In October, ISM Manufacturing PMI dropped to 46.7 from 49 the prior month. The New Orders subindex fell to a 6-month low, and the Backlog of Orders subindex remained deep in contraction territory. The Production and Employment subindexes decreased, while the Supplier Deliveries subindex indicated faster delivery times for the 13th consecutive month. Historically, PMIs have been a leading indicator for future market performance and earnings revisions. Falling PMIs signal the potential for weaker forward returns and negative earnings per share (EPS) revisions.

US Manufacturing Activity Moves Back into Contraction

Soft Economic Data Continues to Rollover

The role of soft data in assessing the sustainability of expansions compares to prior periods similar to today, such as 1996, 1999, 2007, and 2016, where homebuilder sentiment and ISM Mfg PMI signaled expansion.

The analysis showed that the strength of soft data was the difference between sustainable and unsustainable. Focusing on today, the November reversal lower in ISM Mfg PMI and the decline in homebuilder sentiment suggests that the current "expansion" is not sustainable.

Consumers Credit Usage Continues to Rise

October Labor Market Data

The unemployment rate rose from 3.8% to 3.9%, reaching its highest level since January 2022 and approaching the critical 4% level. Our U.S. Unemployment Indicator forecasts a continued rise in unemployment (Figure 3). The UAW worker strike clouded the employment report, with manufacturing employment dropping by 30k due to a 33k decline in Motor Vehicles & Parts. Notably, the 150k job gains were below the 180k consensus estimate, implying the miss was driven by the UAW strike.

However, we do not think the UAW strike caused the rise in unemployment. Initial claims remained subdued in recent weeks, and most states do not allow workers on strike to collect unemployment benefits.

US Unemployment Rises to January 2022 Level

Important Disclosures

This material is provided for general and educational purposes only and is not investment advice. Your investments should correspond to your financial needs, goals, and risk tolerance. Please consult an investment professional before making any investment or financial decisions or purchasing any financial, securities, or investment-related service or product, including any investment product or service described in these materials.

Our Insights