Fed Holds Rates Steady, But Continues to Forecast 3 Cuts This Year

Photo Credit: Rod Long, Unsplash

Weekly Market Recap for March 22, 2024

Despite stronger-than-expected inflation data for January and February, Fed Chairman Jerome Powell anticipates cuts to short-term interest rates in the second half of this year. The central bank is considering two or three one-quarter-point reductions to the federal funds rate, now at 5.25%-5.50%. Indications are that the domestic economy remains healthy, but growth is easing. Though employment has proven resilient, new hires and wage increases are slowing. Housing costs appear to be moderating, indicating better overall inflation comparisons going forward.

Wall Street expects the Federal Open Market Committee to hold interest rates steady at its next meeting (April 30th-May 1st). Most economists and analysts believe rate cuts will be announced in June. Fed officials have stated that data trends will determine actual rate policy. We believe three cuts, totaling 75 basis points, will occur to yearend.

Next Week’s Economic Releases

Dallas Fed Index (3/25)

New Home Sales (3/25)

Consumer Confidence Index (3/26)

Richmond Fed Index (3/26)

S&P 20-City Home Price Index (3/26)

Kansas City Fed Index (3/28)

Michigan Consumer Sentiment (3/28

GDP Price Index (3/28)

Pending Home Sales (3/28)

S&P 500 Index (Last 12 Months)

S&P 500 Technical Composite (Last 24 Months)

March Federal Open Meeting Committee (FOMC) Meeting

As expected, the Fed held interest rates steady this week. The key update was the Summary of Economic Projections (SEP), which now forecasts more robust GDP growth, lower unemployment, and higher inflation than December. While the revisions highlight upside risk to growth and inflation, the Fed's projection for three cuts this year was unchanged. There are numerous ways to interpret the Fed's updated SEP (more robust growth & higher inflation) and dot plot (still forecasting three cuts):

The Fed is willing to tolerate higher near-term inflation. While inflation data is moving in the wrong direction to start this year, the Fed believes the trend is lower and that the bump in early 2024 may be seasonal.

The Fed wants to cut interest rates this year. Interest rate cuts are coming, and whether the final tally is 2 or 3 cuts is inconsequential.

The upward revisions to the 2025 and longer-term fed funds rates indicate that the Fed is still debating the neutral interest rate. There's a thesis that the neutral rate is higher after the pandemic, which we agree with, and the Fed is starting to acknowledge that view.

The Fed's credibility is becoming more questionable.

Chair Powell claims the Fed will be data-dependent, but after raising its 2024 growth and inflation projections, the Fed still expects to cut three times this year. In addition, Powell described financial conditions as restrictive despite evidence they are not.

Change in Fed’s Summary of Economic Projections

Financial Conditions Index

Housing Data Continues to Strengthen

Prices Homebuilder sentiment improved for a fourth consecutive month in March and rose to an 8-month high. Builder sentiment continues to improve as a lack of existing inventory continues to push buyers toward new home construction. In addition, the average 30-year fixed-rate mortgage sits near 6.75%, nearly the lowest level since June 2023. Additional data shows building permits continue to trend higher, posting a fourth consecutive month of growth in February. Housing started rising by +10.7% in February after declining by -12.3% in January, suggesting that January's cold weather weighed on housing starts. Single-family housing starts surging by +35.2% year-over-year, indicating that last year's tightening-induced slowdown is fading. On an annualized basis, the pace of single-family starts was the highest since April 2022 as builders rush to meet robust demand.

Homebuilder Sentiment Continues to Strengthen

Building Permits Continue to Move Higher

Industrial Production Rebounds

Industrial production rose by +0.1% in February after falling by -0.5% last month. On a year-over-year basis, industrial production fell by -0.2%. Manufacturing output rose by +0.8%, and the index for mining jumped by 2.2%. The index for utilities fell by -7.5%, with the decline attributed to above-average temperatures. The gains in manufacturing and mining and the decline in utilities partly reflected recoveries after weather-related disruptions in January. In the durables category, notable increases were recorded in wood products, furniture and related products, automotive products, and machinery. Chemicals, paper products, and textile mill products increased in the nondurable category. The latest data suggests weather played a role in this year's sluggish start.

Industrial Production Rebounds in February

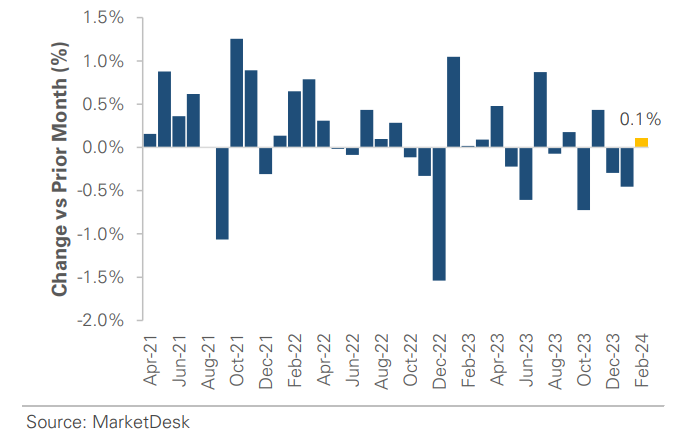

Import Prices Rise

The cost of imported goods rose for a second consecutive month in February, adding to the upturn in inflation this year. The import price index rose by +0.3% following a +0.8% gain in January. Import prices ex-fuel rose by +0.16% after a +0.65% rise the prior month. It was the first back-to-back monthly increase since last summer, as higher prices for consumer goods, foods, feeds, beverages, capital goods, and automotive vehicles more than offset lower prices for nonfuel industrial supplies and materials. For most of the past two years, the cost of imported goods has steadily declined, helping to lower inflation. However, the trend now appears to be reversing, with oil prices surpassing $80 per barrel. In addition, last week's CPI and PPI reports were hotter than expected. The data raises questions about when the Fed will start to cut rates.

Import Prices Ex-Fuel Rise for 3rd Time in Four Months

Asset Allocation Takeaways

This week's FOMC meeting and Chair Powell's press conference removed the hawkish Fed catalyst. The Fed is more concerned about unemployment and an economic slowdown than inflation despite evidence of solid growth, sticky inflation, and loose financial conditions. The Fed's policy views continue to favor stocks over bonds, which offer exposure to higher nominal growth and protect against inflation.

Important Disclosures

This material is provided for general and educational purposes only and is not investment advice. Your investments should correspond to your financial needs, goals, and risk tolerance. Please consult an investment professional before making any investment or financial decisions or purchasing any financial, securities, or investment-related service or product, including any investment product or service described in these materials.

Our Insights